This is a place for a "road side analyst" to share his view about the Macro and Micro as well as some stock pick and outlook..

I Seldom write but when I write I will make it right and make it count!

Market had started to breath negatively for yesterday and

add up with the shoot down of Russian fighter jet had pushes the sentiment even

worst. On the other hand, the shoot down had causes the oil price to shoot

which had in turn causes RM to appreciate. This had resulted sell down in export

counters in the market today.

As we have mentioned before, the high volume traded in the

market is showing the market is hot and again, the fall of small cap and those

export stocks had again proven our that our volume theory works.

We have saw 3 of our holding companies had announced their

quarter result and the results are great. However the sentiment is bad and we

have saw huge sell down to these stocks where some of it had hit our run road

price. To those weak holders, please follow your trading plan and for us, we

are still looking at these stocks as they have value within.

Remember, U may RUN ROAD today but don’t forget to look back

at it again once it is oversold as it will be dirt cheap to invest!

Some of the readers had started to ask Big Canon when we

will re-enter the stock. Well, we will wait for it to be oversold and that’s

the time we add in our position.

As for tonight, we don’t have much to highlight but U may

read our update on 2 of our holdings:

To our readers out there, do not lose faith to the market as

ups and downs are just a normal cycle, stock with value will always move up

when the time comes. Be confident and trade according to plan.

Last but not least, this is the time to observe whether who

is swimming nakedly. Time to hunt for gold mine! XD

D&O had suffered a bad sell down today however the

volume was low, so what’s the reason behind? Well, we believe there are 3

possibilities.

1.Bad sentiment overall the market.

2.Quarter report players are afraid of bad quarter

report

3.The insider wanted to collect some cheap tickets

It’s hard to tell by now whether what is the root cause and

only time could tell. However, let’s analyse the Quarter report as it is a

decent surprise to us. The company didn’t slipped into red as we afraid yet

they showed better result compare to the same quarter in 2014.

Note B1:

3 rd Q 2015 versus 3rd Q 2014

Turnover grew 15% year-on-year to RM122.2 million, propelled

by a 34% growth in the Automotive Segment to RM67.7 million. Revenue of the

Non-automotive Segment, comprising primarily the General Lighting Segment, was

2% lower at RM54.5 million.

Gross profit margin in the current quarter improved

significantly to 20% compared to 13% a year ago on favourable sales mix change

and a strengthening US Dollar against the Malaysia Ringgit. Consequently, the

Group recorded significantly better profit before tax of RM6.2 million compared

to RM0.7 million a year ago.

9 months 2015 versus 9 months 2014

Despite a 27% growth in the Automotive Segment, turnover for

the first nine months dipped marginally by 1% to RM326.1 million as a result of

a 26% decline in Non-Automotive Segment to RM132.1 million. Revenue of the

Non-Automotive Segment was adversely affected by management’s decision to phase

out mid-power LED packages.

The Group posted an improved gross profit margin of 19%

(9M2014: 14%) mainly as a result of a favourable change in sales mix and a

stronger US Dollar versus the Malaysia Ringgit. The Group achieved a profit

before tax of RM15.0 million compared to RM4.6 million a year ago on higher

margin.

Note B2

When compared to the preceding quarter, revenue in the

current quarter increased by 8% to RM122.2 million. The Automotive Segment

registered a 7% increase to RM67.7 million, while the Non-Automotive Segment

expanded by 10% to RM54.5 million on higher COB sales. Gross profit margin

improved from 17% in the preceding quarter to 20% in the current quarter under

review mainly due to an increase in sales volume, better sales mix and a

weakening Malaysia Ringgit against the US Dollar. However, profit before tax at

RM6.2 million was only marginally better quarter-on-quarter (2Q2015: RM6.1

million) as a result of unrealized forex loss from US Dollar denominated

payables and higher customer claims in the current quarter.

Note B3

Commentary on Prospects

The overall subdued global economic performance is not

expected to improve anytime soon. Nonetheless, LED sales to the automotive

industry is projected to continue with its growth momentum, underpinned mainly

by rising LED adoption in the exterior and interior display applications.

Through product innovation, competitive pricing and recent

strategic collaboration with Taiwan’s leading LED wafer manufacturer Epistar,

management is optimistic that Dominant would be able to further strengthen its

market share position in the burgeoning automotive sector.

Competition in the Non-Automotive Segment, namely the

General Lighting Segment, on the other hand will likely remain stiff on both

cost and pricing pressure. To reduce overhead costs and improve production

efficiencies, management has decided to consolidate and streamline its

manufacturing capacities.

The recent 10% equity injection by Epistar into Dominant in

November 2015 has significantly strengthened the Group’s balance sheet,

providing the Group adequate resources to further expand its LED business.

Barring any unforeseen circumstances, management is optimistic the performance

of the Group for the year will be satisfactory.

Something to highlight

1.Note A15, where it mentioned Dominant had

received full cash in 9 November 2015, which mean they will put the one off

profit in next quarter.

2.If u look at the Current asset, we saw that the

cash of the company had jumped from RM29m to RM57m. However, the company is

still not a net cash company yet and we believe this cash is not from the

selling of Dominant as we still don’t see any cash from the cash flow from

investment as well as gain on disposal of interest in an associate.

3.Looking at Note B12, which is the material

Litigation, it had clearly stated that the company had placed the sum of

compensation RM13.45m as trade payable. This is because they have appeal for

the case and the hearing is on 18 Feb 2016 which the court case will be crucial

to decide whether they have to pay that RM13.45m. If they win the case then

they will not need to pay this RM13.45m and they are able to get back another

RM12m which has been classified as contingent liability.

Summary

1.The Revenue had grew 15% compare to last year

and grow 8% compare to last quarter. PAT of the company is 416% higher compared

to last year but 9% lower compared to last quarter. The lower profit were due

to unrealized forex loss from US Dollar denominated payables and higher

customer claims in the current quarter. In short, the business is still

growing.

2.The company has yet to factor in the pending

result of the material litigation which will be deciding on 18 February 2016.

On the other hand, they have another case that pending announcement on 16th

December 2015

3.Company will be having a one off gain by next

quarter.

4.The cash position of the company had increased

significantly

5.The company is still healthy where it is still

worth looking at after the poor sentiment.

The bad market sentiment had caused the most of the stock

tumbled and we saw OCNCASH dropping as well. However, OCNCASH had finally

release their quarter report this evening and the result shows 600% increase

from preceding year and is flat compare to last quarter.

What is so special with the company quarter report?

From note A8, we can see that

1.The growth of the company came from Hygiene

segment where the Felt segment remain flat.

2.The growth is from Japan, Indonesia and Thailand

(Please check the photo attached)

3.The 9 months revenue of the company grow by

12.23%

From note B1, we can see that

1.The increase in revenue and profit was due to

strengthening Rupiah

From note B3, Prospect for Year 2015

The management anticipate the group’s performance for the

financial year 2015 to be better than 2014.

Surprising Dividend,

Company proposed interim dividend of RM0.007

Summary,

1.As we mentioned in our article before this, we

saw growth from Thailand, Indonesia and Japan.

2.Company get marginal benefit from the

appreciation of Rupiah

3. Company

had made Rm4.913m for whole year in 2014 and now they made RM7.085m net profit

for the past 9 months in 2015. This is RM2.7m higher than last year and company

had just QUALIFY THEMSELVES FOR LISTING BOARD CHANGING REQUIREMENT.

4.A surprising dividend proposed by the dividend.

As we can see, the company is still doing well and healthy

and it is still undervalue by now (according to our valuation in the previous

note). The company had given interim dividend to compensate the shareholders.

The sell down today was due to the bad sentiment hence any weakness is our

chance to invest further.

There are a few important things took place today:

1st Saudi said that they are willing to cooperate with fellow producers to stabilize prices. This had sent the oil price higher in US morning session.

Source: http://www.marketwatch.com/story/oil-futures-rebound-after-saudi-arabia-says-will-work-to-stabilize-prices-2015-11-23?dist=beforebell

2nd During the visit of China Premier, he said that China will help Malaysia by buying more Malaysian government bonds and give the country a 50 billion yuan (US$7.83 billion) quota to invest in Chinese stocks and bonds, as it looks to strengthen ties with Southeast Asia.

Source: http://www.theedgemarkets.com/my/article/china-buy-malaysian-bonds-offers-investment-quota-southeast-asia-push

3rd 1MDB sell their power business to Chinese-led consortium for equity value of RM9.83b.

Source: http://www.theedgemarkets.com/my/article/1mdb-sells-power-business-chinese-led-consortium-equity-value-rm983b

Summary: The 3 news above gave us a feeling that Malaysia might start to move away from the major woes whether it is fundamentally or politically. Why?

1st The fall of oil price had causes Malaysia to suffer as Crude oil is 1 of the major income for Malaysia.

2nd China will help us by buying up our bond to provide liquidity to Malaysia, this can help especially when we are facing capital flight.

3rd The selling of 1MDB assets might signal a good start to put an end to all the political and financial saga.

Though the 3 things above are quite positive to us, but we are still obsess with the Volume in FBMKLCI.

As we can see the total shares traded had hit 2.9b again for today and we insist that players should be careful as the market is very HOT. There are rotational play for Penny stocks from XOX, to Instaco and the latest 1 is Genetec where the turnover rate for today is already 44.8% and this 44.8% is telling that 44.8% of the shares were traded and changed hand.

THIS IS MADNESS!

However, Big Canon has no crystal ball to predict when the music will stop, and hence managing your risk with a proper game plan is what U should have.

We don’t have individual counter to highlight tonight, but you can still check out full article of OCNCASH – Ocean of CASH? To know more about the counter.

http://bigcanon.blogspot.my/2015/11/oceancash-0049-travelling-towards-no.html

May all the HUAT be with us!

Regards

Big Canon Finance

Oceancash is an Ace market counter that we have chose on last Wednesday (18/11/2015) where we have a TP of 10% above our cost, but we've decided to increase the TP and the article below will explain the reason behind.

The nature of business

OceanCash Bhd is a company that manufactured "Felts" and "Non-Woven" materials.

1. OceanCash Felts:Manufacturing and distribution of resinated felts and thermoplastic felts for thermal and acoustic applications.

These items are basically use in our car. U can check the website below to know more: http://www.oceancash.com.my/OurSubsidiaries.html

2. OceanCash Non-woven: Manufacturing and distribution of thermalbond, airthrough and specialty nonwoven fabrics for hygiene applications.

These items are basically use in our hygiene item such as Pampers and Mask. U can check the website below to know more: http://www.oceancash.com.my/OurSubsidiaries-Nonwoven.html

Fundamental

Revenue:

The table above shown clearly that the revenue is growing steadily.

Net Profit:

The net profit for the company has been growing steadily for the past 4 quarters.

Looking at the latest quarter report, we can see that the retained earnings of the company is 1.28times larger than Share capital. In this case, this mean that the company is having sufficient financial muscle to give a 1 to 1 bonus issue in near term.

We believe this company has high potential on giving bonus issue in near term.

Theme:

1. Benefit from Strengthening USD

From the latest Quarter report, we can see that 70% revenue of the company are from foreign countries. As a result, we believe the company will have a boost on the coming quarter result as that was the worst time for Ringgit.

In the annual report of 2011, we can see that the company mentioning the cost of high crude price is one of the reason for high raw material cost. As a result, we would have to make an assumption here that the company will have lower cost of material as the crude oil price is much lower by now. (We have saw the same situation that happen to most of the plastic related industry recently)

Looking at the chairman statement of Annual Report 2014, we can see that the company are Growing!

Looking at point no 1, we can see that they are relocating their production line in Indonesia and there is an increase from 1 production line to 2 production line in Indonesia which is expect to be fully operated in 2016

Point no 2, the company is expanding into Thailand.

Point no 3, the company have got new client (increase in demand) where they will modify their production line to increase capacity (increase production) in order to fulfill the demand.

Point no 4, the company is trimming down their non-performing business which helps to boost the efficiency of capital by cutting cost.

4. Changing Listing board from ACE to Main Market

As we know, the 1st 2 requirement to change board from Ace to main market is

1. Having cumulative of Rm20m in 3 to 5 years time

2. The earning for that last year should be above RM6m.

Looking at the situation above, we can see that the company had made RM16.178m in the past 4 years, which mean the only thing to qualify them from changing board is making RM6m by end of 2015 financial year.

Looking at the current financial year, we can see that they have made RM4.671m in the 1st 2 quarters, which mean they need another RM1.4m then they will be qualify for the change board listing. So the current quarter and the next quarter result will be crucial to the company.

Valuation

With using the EPS of the past 2 quarters which is 2.1c, hence our annualized EPS will be 4.2c.

As per the closing price of OCNCASH on Friday, which is 44.5c, we can easily come to a valuation of 10.59 times PE.

Looking at the counter of related industry such as NTPM with 17 times PE and Halex with 28 times PE and the PE of OCNCASH of 10 times, we can easily get an average of 18 times PE for the industry.

To be conservative, we give Ocncash a PE of 15 times after a 20% discount from the industry, we can see that a 15 times PE Valuation will suggest that OCNCASH should be trading at 63c.

Technical Analysis

The share price had hit historical high on last Friday, which mean the share is now in an area of no resistant. That is why we said the counter is now traveling towards no man's land.

RISK

Seriously, we can hardly see any risk other than seeing the company had turn from a net cash company to a non-net cash company. However, this is a very normal thing as the company has to borrow money to expand their production.

1. The risk we can think of is, the result might turn out to be not as positive as we think. As a result we will have to set RUN ROAD price once things had turned against us. We will set our RUN ROAD Price at RM0.41 as it is the place where we saw the stock started to moved.

2. Company failed to qualify for change board listing. If this were the case, then RUN ROAD is the only way.

Summary

1. Company is growing healthily by having steady Revenue and Income Growth.

2. Company is potential for bonus issue.

3. Benefit from strengthening USD

4. Benefit from low crude oil price

5. Growth contribution from Indonesia and Thailand as well as new customers.

6. Potential for changing listing board from Ace to Main market.

7. Cheaper Valuation compare to peers and industry average.

8. No more resistant from technical analysis wise.

As a result, we have adjusted our short term TP from RM0.465 to RM0.50 while mid term target of RM0.60.

However, all of this TP is subjected to their coming quarter earnings, if the coming quarter earnings that will be announcing in November didn't do well then we will have to RUN ROAD!

The minutes of FOMC meeting on October had indicate that FED’s

are ready for a rate hike on December. US market had rallied after then, could

this an indication of the market are ready for a rate hike? Well, we believe it

is still too early to conclude anything and close monitoring is important at

this stage.

US market had rallied last night while European market and

East Asia were having rallies but WHY IS FBMKLCI NOT HAVING RALLY? We saw RM

had strengthen today but it is worth noting that FBMKLCI is not having rally

today which is not align to most of the market. Other than Malaysia, we found

that our regional market such as Singapore, Thailand, Philippines and Taiwan

are not having rallies. WHY? Well, Big Canon is not sure why as well, however IT

IS IMPORTANT TO KEEP MONITORING and BE AWARE!!!

Other than the 2 issues mentioned above, there is another

issue that worth noting is the total shares traded today. The total shares

traded today is 3.425b shares which is the highest after August 2014. HENCE,

BIG CANON WOULD LIKE TO ISSUE STRONG WARNING HERE! IT doesn’t mean the market

will drop immediately but THE RISK OF GOING DOWN IS HIGHER NOW, PLS TRADE WITH

EXTRA CARE AND SET UP A TRADING PLAN and FOLLOW THE PLAN STRICTLY. A PROPER RUN

ROAD PLAN IS IMPORTANT WHEN THINGS ARE NOT RIGHT.

There is not much stock to highlight recently as we are now

spending most of the time doing study about the quarter results and digging GEM

through it. U may PM us and justify to us if you think U found GEM.

Solutn stock that we choose on 6th November for

result play and it had strike out TP of 0.45 on 17/11/2015 which we have

harvest 75% of our position and left with 25% for the result play.

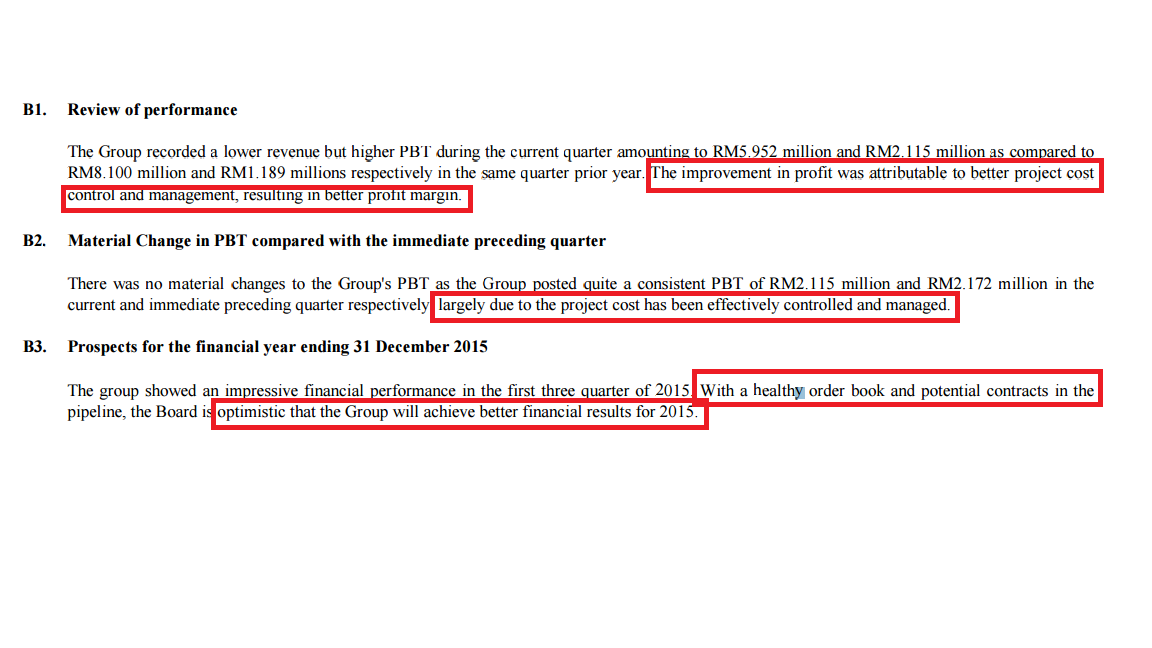

Solutn had announced their Quarter result today where we saw

the Profit jump 110% y-o-y from RM0.7m to RM1.473m, however the profit slide 3%

q-o-q from RM1.52m to RM1.473m. The revenue drop 26.52% y-o-y from RM8.1m to

RM5.95m while rose 1.95% q-o-q from RM5.838m to RM5.952m.

Why is the revenue drop but profit able to move up?

Looking at the quarter report

Note B1 Review of performance,

B2 Material change in PT

We can see that the company don’t have any one off gain, but

it was due to higher margin and better cost control (highlighted in the photo).

The Balance Sheet of the company, we can also see that the company is a net cash company (excluding trade payables) with RM16.925m which translate to RM0.0847 per share.

As what we can see, the company is still doing well though

it doesn’t have a very bombastic quarter result. However, we will still

maintain our TP of RM0.45 for momentum play and we have a trailing RUN ROAD

price of RM0.41. We have shifted our RUN ROAD Price upwards from RM0.38 so that

we can exit the counter with profit.

As we mentioned before, we will have to monitor closely whether how will the market react to the changes in U.S. after the unemployment rate and non-farm payroll. As for tonight, we saw U.S. inflation rate where the core inflation y-o-y grow 1.9% while inflation rate m-o-m grow 0.2% which is higher than expected.

Source: http://www.tradingeconomics.com/calendar

We notice that US market had rebounded strongly last night where it has a bullish engulfing for both DJIA and S&P 500 as well as a big white candle for Nasdaq, however we still have to monitor whether the index will have another green bar tonight to show the validity of the bullish engulfing. However, it is worth noting that the index is still below MA10 which has yet to get back to bullish trend and Nasdaq is still below their 5000 points when we were writing this.

FBMKLCI has got a gap up graveyard which is still below the MA10, we have to monitor whether it will close the gap or not where it will not be good if today’s gap were seal. Looking at the index, we believe it is at cross road now where it is undecided with its direction. This is due to strong support were seen in past few days, however, the surge today was well capped too.

Though the market has not direction, but our stocks are doing pretty well where they have Kaboooom yesterday and today. As on 6th November, we were still having 4 stocks on our portfolio which is D&O, Tomypak, Opcom, and Solutn. (Please check back our announcement on channel by 6th Novmember)

3 out of 4 have Kaboom yesterday and today! As a result we will update u our position as per today.

Entrance Date: 3/11

D&O (ST)

Cost: 0.39/ Expect 0.43/ Anticipation: 10%/ highest: 0.43/ Closing: 0.415

Kaboooom! Harvest after hitting our TP!

Harvest: 75% of our position

Tomypak (MT)

Cost: 2.45/ Expect 2.80/ Anticipation: 15%/ Highest: 2.97/ Closing: 2.88

Kaboom! Harvest after hitting our TP where it give another 3.6% or 10c for consolations!

Harvest: 75% of our position.

Entrance Date: 6/11

Solutn (MT)

Cost: 0.40/ Expect 0.45/ Anticipation: 10%/ Highest: 0.45/ Closing: 0.44

Kabooom! Harvest after hitting our TP!

Harvest: 75%

That’s the position that we have harvest but there is a bad call where we have still yet to dispose.

So far 7 out of our 8 picks had Kabooom!!! They are 3A, TekSeng, D&O, Tomypak, HupSeng, Solutn, and Luxchem. We would like to Congratulates those followers that who made from these Kabooom counters and we promise we will find more good counters and share it to our readers!

Last week we asked our Squad members to be precautious and

be aware as the market is now anticipating rate hike from the FED in US. As we

can see, the US dollar index is now hitting 99.5 which is about to touch 100

while their 10 years yield is hitting 2.351%, these are sign of market betting

on a rate hike.

As we mentioned last week, we can’t control the market but

all we can do is just monitoring the direction and react accordingly. All we

can do now is monitor whether can DJIA breach new high again and it is

important to break 18k as it is a very strong resistant at this level. We might

not be able to see it breach 18k in a short term if the market really think

there will be a rate hike soon. On the other hand, we have

Big Canon would like to share some history that happen not

long ago with all the Squad members. Looking back in 2014, we’ve met a

situation in Malaysia where we have got a rate hike for OPR from 3% to 3.25% on

10 July 2014, on the other hand our index had hit historical high of 1896 on 8th

July and our index never able to breach new high after the rate hike. As we can see, the rate hike had absorbed the

liquidity in the market which indirectly causes the market not to break new

high.

Our question is “will this happen to US market after rate

hike?

As for Bursa Malaysia, it is important to monitor whether it

can breach 1700 points again, if the index failed to hit it and fall below 1660

then it might be a time for Put Warrants. We are currently directionless but we

are cutting down our shareholding and increasing our cash position. However, we’ve

started to monitor put warrants.

The put warrant that we would monitor is H5, H27, H21 and

HW. Please notice that these 4 put warrants are having SKY HIGH PREMIUM,

however we like H5, H27 and H21 because it is cheap enough in terms of price though

it is having sky high premium. The reason behind is that these cheap put

warrant will always get attack by banker when the market tumble and the

percentage of return is higher since its cheap but NEVER FORGET HIGH RISK HIGH

RETURN too! The reason of HW is because it is having longer maturity.

WARNING: PUT WARRANT BEING MENTIONED IS HIGHLY SPECULATIVE

AND IS ONLY FOR MONITORING AT CURRENT SITUATION. PLEASE BE AWARE OF THE RISK WITHIN.

THE RISK OF THIS INSTRUMENT IS TOO DAMN HIGH!

About D&O that we highlighted on Sunday, we have written

down the reason we like it and also the risk within in our blog. You may read

it at the link below.

D&O Green Technologies (7204) - The 2nd last L.E.D Dragon

awaking

Highlight for tonight is a bit special as we are going to highlight

a stock that is on its way to listing in Bursa Malaysia and its KIM TECK CHEONG

(KTC), this counter is undergoing IPO process where the due date is on 12

November before 5pm. We strongly encourage Squad member to look into the

company.

Before ending the day, Squad members are advised to exercise

more caution and try to be safe on each trading as we feel that there are

storms coming in our way. It’s better to be safe than be sorry.

Have u change the light bulbs in your house to L.E.D? Well done if your answer is "yes" as u care for the mother nature as well as the money in your pocket!

So how shall we benefit from this trend other than just buying and changing L.E.D bulbs? Investing in those L.E.D related company is an answer.

L.E.D a trend that no one can resist, hence, it is call a MEGA Trend.

Why? L.E.D. saves electric and having longer life spend which helps to save on ur electric bills as well as your money in pocket. On the other hand, it is more environmental friendly compare to the old technologies.

As a result, we have saw lots of the companies that are related to L.E.D rocket up tremendously.

For an example: IQGroup, Ulicorp, Success, Elsoft, Penta (related) and MMSV (related). As u can see, those mentioned above had moved a lot save for D&O(7204) and Tecfast(0084). Don't know when will Tecfast awake though they have done some corporate exercise recently.

So why are we looking at D&O?

1st The price had started to moved recently, but why? Why is it moving? Any good supporting behind?

As we can see, the profit of the company is growing and getting higher. However, is this a one off item that causes the profit to shoot up?

Dissecting the Quarter Report

Let's take a look at their Quarter result ended on June 2015 which was announced on 19th August.

Looking at the Income statement, we can't find any other income being stated in it which means the profit of the company are all from operation and not related to 1 off disposal.

So where do this profit come from?

We have to check the notes at section B of the QR to know more about the company, only if they are willing to tell us.

Looking at the note above, now we know 2 key factor that brings growth to the company's profit:

1. The company had shifted their focus from low margin non-automotive towards higher value and margin product. This had increase the efficiency of company by increasing their margin.

2. The company had benefited from the strengthening USD and this have increased their profit margin and boosted their bottom line.

How does this company benefit from USD?

We check back at note A10

As u can see, the company is exporting their products to Europe and USA and that makes up 25% of their Revenue. As a result, the stronger the USD is, the better to the result of the company.

3. After knowing the reason of why the profit shot up then its time to check about the sustainability of the result. How shall we check that? Look at the prospect section by the management in Quarter Report.

The management think that the market is challenging due to economic slowdown, however company is trying to mitigate it by doing cost saving n restructuring to increase the efficiency.

On the other hand, the company will also shift their focus from those low margin product to those high tech product as well as high margin product to increase the profitability and to focus more on automotive industry.

As we can see above, there are the parts in car that will need L.E.D which had create lots of demand towards this industry.

This note is very important and it tell us where are the company heading to. Let's take a look at the prospect commentary for the 1st quarter.

In the note for the 1st Q QR, the management had already told us that (highlighted in blue box) the company is having lots of sales order from clients and they are optimistic about the coming quarter reports. As a result, we saw that the company had made more profit than before, hence dissecting Quarter report also very important.

Let me quote 1 of the famous guru 冷眼:书中自有黄金屋! this mean there are treasure hidden in the book, and yes, the treasure are hidden in the Quarter report and Annual report for investors like us!

Its not the end even after looking at the Quarter Report, we have to see the recent announcement from Bursa Malaysia website too!

What catching our eye is the Share Sale Agreement on 28th September where

TRANSACTIONS (CHAPTER 10 OF LISTING REQUIREMENTS) : NON RELATED PARTY TRANSACTIONS PROPOSED SUBSCRIPTION OF 11,000,000 NEW ORDINARY SHARES OF RM1.00 EACH IN DOMINANT OPTO TECHNOLOGIES SDN BHD ("DOT"), A 68.71%-OWNED SUBSIDIARY OF D & O GREEN TECHNOLOGIES BERHAD ("D&O") BY EPISTAR CORPORATION ("EPISTAR") ("PROPOSED SUBSCRIPTION")

This means Epistar will be paying D&O RM64.845m for 10% DOT's new issued shares.

2nd Who is this Epistar Corp? and what's the benefit of selling this shares to them?

To know more about Epistar, please watch the video below:

You may also visit their website to know more about this company.

http://www.epistar.com.tw/index_en.php

Looking at note 4 and 5, we understand that Epistar is 1 of the supplier for DOT and they are well known where it will be a strategical move to let Epistar join the party so that DOT may leverage on Epistar strength to grow further.

On the other hand, this can help to increase working capital for DOT too.

As a result, we understand that this will be a good move to sell 10% share to Epistar which helps to increase the potential of DOT. This is a strategical move to the company!

3rd After selling, what's the benefit of D&O?

According to note 8.3, the share sales will bring RM31.36m to D&O which will surely boost up the profit of the company by this year.

On the other hand, this will also increase the retained earning and Net asset per shares of the company as well as lowering down the Gearing of the company. These are all a boon to D&O.

4th After selling the 10% stake, will that dilute the profit of the company? So does that mean the profit of D&O will come down?

Our answer is yes and no.

Yes, is because assuming the company has no grow in its profit then it is certain that their profit will be diluted.

However, we can see that the PATAMI of the company is growing. As a result, it doesn't mean that D&O will have lesser profit after selling stake as long as the profit of DOT is growing. By having Epistar to participate in this company strategically, we believe the D&O's profit might grow even more due to the new partner!

5th When will we able to see the profit?

There is an announcement for company on 9th November 2015 which is still hot n spicy.

As we can see, D&O had satisfied all the requirement of the SSA and have got RM64.845m in their account now. Kaching Kching!

However, looking at the date of completion which is 9th November, hence we believe the profit of RM31m will not reflect in the 3rd Q QR that will be announcing in November due to the cut off date, however, it will reflect in the 4th Q QR which will be announcing in February.

RISK of D&O

We cant just keep looking at the good things, we will have to look at the risk of the company too. What we found that will risk our position is that the Material Litigation of the company.

The company have got a material litigation issue announce on 5th June, which is :

There are 2 important things in this announcement.

1st DOT had lose this court case and they will have to pay compensation of RM13.45m + RM8.28m, however, D&O had already accrued that RM13.45m in its previous financial report hence we will only see an impact of RM8.28m as a 1 off cost in this coming quarter result.

Warning! This might possibly turn D&O 3rd Q result from positive to negative.

2nd That's not the end of the court case, D&O in turn had Sue the current "plaintiff" back, which we will have to pray hard that DOT will win this coming court case. This might be something good for us.

Chart wise, we can see that the price is still holding well even its the T4 after the highest volume, which mean those buyers who came in are a strong player that can hold tickets. As a result, the buyers able to hold and not prepare to sell, that's mean new buyers have to buy with a higher price.

We can also see there is a floor at around 0.365, as a result, it will be our floor supporting point and it is also a place for us to decide whether to RUN ROAD alnot. We will RUN ROAD if the price fall belows 0.365 as it had violated the floor supporting.

Summary:

1st : D&O is a rising STAR where we can see it is benefiting from L.E.D MEGA TREND and also benefiting from the automotive industry.

2nd: D&O is benefiting from weak Ringgit

3rd: D&O had sold part of its subsidiary shares to EPISTAR which helps the company to generate one off gain RM31m which we believe will reflect in the 4th Q result.

4th: The risk of D&O is, they will have a 1 of cost for compensating the counter party after losing the court case, the amount is around RM8.38m inclusive of the fee. This might causes weakness to the share price.

5th: DOT is in another court case where this time they are the plaintiff and "sue" those who "sue" them, and we will have to wait and monitor closely the outcome. Let's hope that they can get back the RM8.38m from them.

6th: Technical Analysis looks intact, however we will run road if goes below 0.365

Conclusion:

Though the court case might affect D&O 3rd Q's result and might even make them lose money, however, in long run, this company is still having more potential than the risk of 3rd Q. It is a counter that we can really look into.

Disclaimer: The content on this site is provided as general information only and should not be taken as investment advice. All site content, shall not be construed as a recommendation to buy or sell any security or financial instrument. The ideas expressed are solely the opinions of the author. Any action that you take as a result of information, analysis, or commentary on this site is ultimately your responsibility. Consult your investment adviser before making any investment decisions